Invest

Market

Stock markets were generally strong in 2017, driven by good macroeconomic conditions and continuing low interest rates which encouraged strong cash inflows to the markets. 2017 saw an increase in the scale of passive investing through ETFs, which meant that the upturn was principally driven by the largest companies both globally and at the Nordic level. At the sectoral level the most notable change was seen in the retail sector, where the performance was negative. Shares in many smaller companies produced a good return in 2017, but this was largely the result of positive company specific developments and so differed from the performance of large companies where good returns were mainly the result of the absence of bad news.

Return

Ferd Invest’s portfolio produced a return of 6.2% in 2017, which is 12.4 percentage points less than our benchmark index. The investments that played the largest role in this underperformance were Norwegian, Opera Software, HM, ThinFilm and Cxense, and the underperformance also reflected the negative impact of weaker NOK and SEK exchange rates. Norwegian and Swedish investments accounted for approximately 80% of the portfolio over the course of year. Ferd Invest’s best performing investments in 2017 were Novo Nordisk, Hexagon, Thule, Stora Enso, Dometic and Modern Times Group.

Ferd Invest holds a concentrated portfolio, and its active share score is as high as 90%. This means that only 10% of the portfolio matches the benchmark index, and accordingly one must anticipate significant variation in relative return from time to time, particularly when there is little correlation between individual shares. The objective for the portfolio is to hold a concentrated portfolio based on individual investment decisions without seeking to replicate the benchmark index composition to any particular extent. This approach seeks to achieve a higher than market return over the longer term through good selection of individual shares. In a year such as 2017 where the portfolio had a clear overweight of shares that produced a weak return, the underperformance relative to the benchmark index is likely to be significant, and in 2017 this was further aggravated by the strong upturn seen for the stock market as a whole.

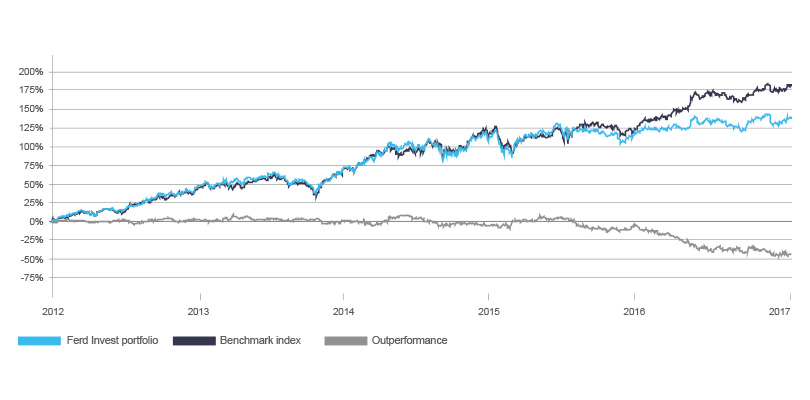

Rolling five-year return

Over the last five years, the Ferd Invest portfolio has achieved an average annual return of almost 17%. This is a very sound return and higher than might be expected in a period of relatively slow economic growth and low inflation. Nordic stock markets have also performed strongly over this period, with an average annual return as high as 20%. As the chart above shows, the benchmark index has pulled ahead of the Fred Invest portfolio over the course of the last 12-18 months, and as previously mentioned the main explanation for this is that we have held too many individual shares where the return has not yet kept pace with the market.

Portofolio

The market value of Ferd Invest’s portfolio at the close of 2017 was NOK 4 billion. The portfolio’s investments are divided between the three Scandinavian stock markets, as well as the Finnish stock market. The largest investments at the close of 2017 were Autoliv, Novo Nordisk, Nokian Renkaat, Norwegian Air Shuttle and Aker Solutions. Ferd’s capital allocation transferred NOK 1.5 billion out of the Ferd Invest portfolio in 2017.

Organisation

The Ferd Invest team currently has two members, Lars Christian Tvedt and Nicolay Mylén. Are Dragesund moved to Ferd Capital in August 2017.